Understanding the natural gas (over)reaction to COVID-19 and oil prices

Most natural gas market observers believe that the COVID-19 pandemic will result in a decline in the production of associated gas due to the collapse in oil prices and the slowdown in drilling activity, as well as a decline in demand. Based on the behavior of the futures market, most participants in the natural gas market expect the decline in natural gas production to be more significant than the decline in natural gas demand.

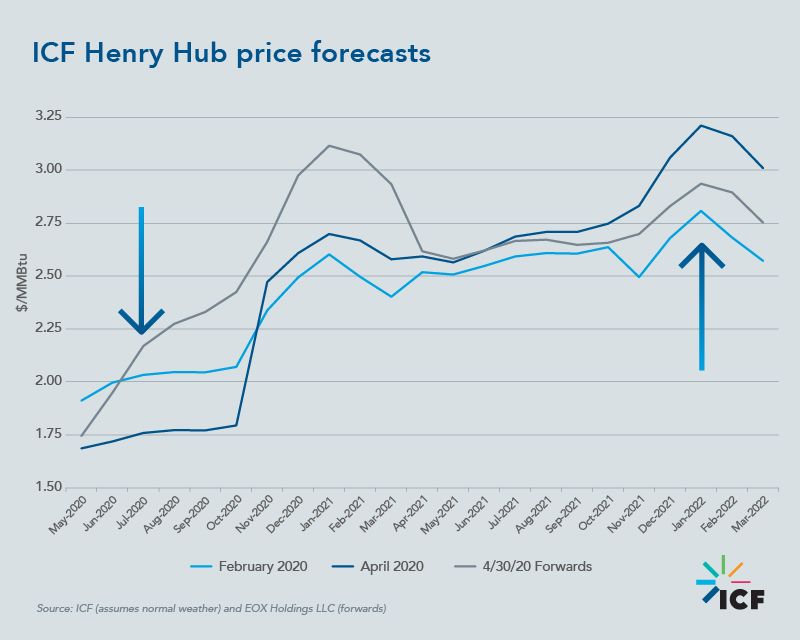

ICF believes the market has gotten this balance wrong. ICF is currently forecasting that the Henry Hub forward curve for this upcoming winter is, under normal weather conditions, overpriced.

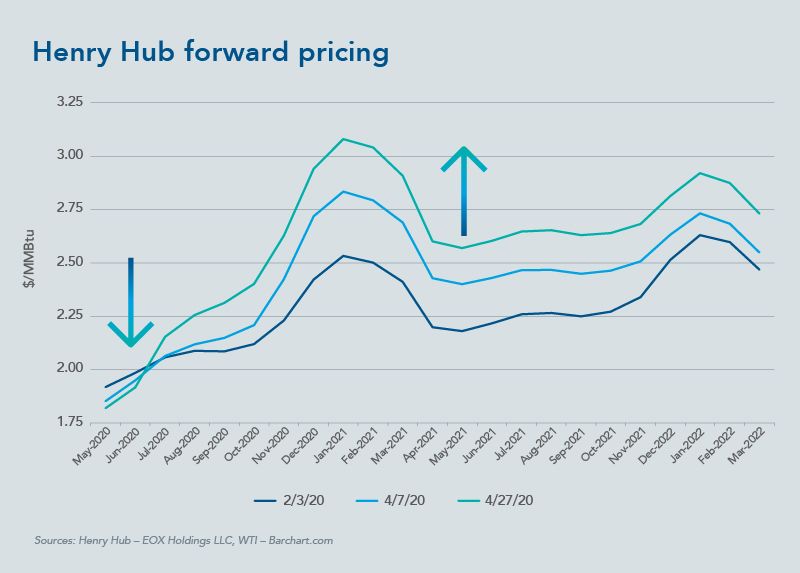

Over the past two months, the Henry Hub forward curve for this coming winter (November 2020 to March 2021) has increased by $0.50/MMBtu. The market now expects the Henry Hub natural gas price to be above $3.00/MMBtu in January and February of 2021. This would be a drastic change from the $2.00/MMBtu average spot price for January 2020 and from the roughly $2.60/MMBtu price that was expected for January and February 2021 as recently as the beginning of February 2020.

Outlook for declining natural gas production

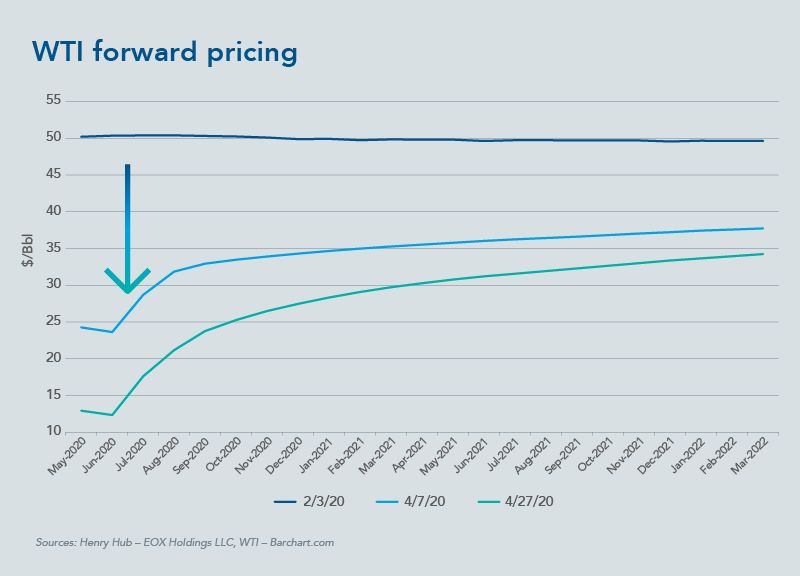

The increase in natural gas price expectations is directly tied to the recent decline in oil prices. The West Texas Intermediate (WTI) crude oil forward curve, as of April 27, 2020, shows sustained low prices of below $30.00/barrel through December 2020.

The collapse in oil prices is the outcome of a dramatic reduction in petroleum product demand due to the COVID-19 pandemic, combined with a global oversupply of crude oil. This collapse is expected to lead to significant reductions in North American oil production, as well as a corresponding decrease in associated natural gas production from regions where natural gas production is a byproduct of oil production.

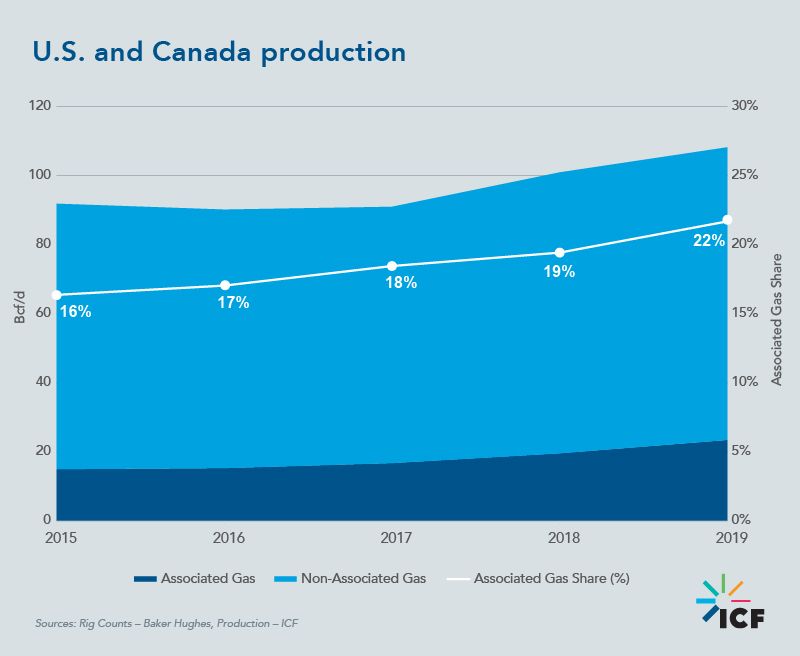

The link between oil production and natural gas production has been increasing in the last few years due to the rapid pace of associated gas production growth in the United States and Canada. This growth has allowed the share of total production for associated gas to grow every year for the past decade.

However, total associated gas production is still only 22% of the total natural gas production in the United States and Canada. This means a significant decline in associated natural gas production will have only a modest impact on the overall natural gas production.

At current prices, the associated natural gas production is adding significant value to the oil wells with associated natural gas. As a result, the value of production from the oil wells with large volumes of associated natural gas is expected to be higher than the value of oil wells with limited or no associated natural gas.

Although many oil producers have already announced oil well shut-ins in several plays like Bakken, Permian, Eagle Ford, and other regions, ICF expects that the drop in associated gas production will be slower than what the market is anticipating, thus limiting the increase in natural gas prices this winter.

Modest, seasonal declines

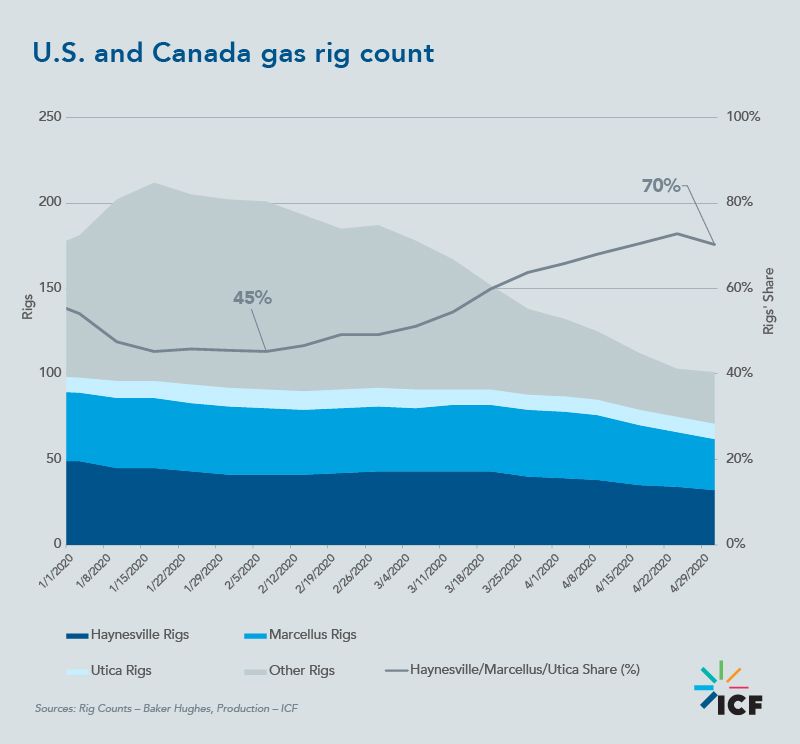

Despite the relative stability in natural gas prices, non-associated natural gas production is also expected to be down from the previous forecasts. Natural gas exploration and development activity has been declining along with oil exploration and development activity. Total gas-directed drilling activity (measured by rig count) has dropped by more than 50% since the start of the year. However, much of this decline has been in western Canada, and reflects standard seasonal activity.

In the other major natural gas plays, the rig decline has been more modest. Non-associated gas production in key areas like the Haynesville play (close to the Gulf Coast demand center) and the Marcellus play (close to the Midwest and East Coast demand centers) will persist.

This persistence is currently reflected in rig counts in the United States and Canada, which have the Marcellus and Haynesville rigs each accounting for one-third of active gas rigs, and the aggregated Marcellus, Utica, and Haynesville rigs comprising 70% of the total.

At current futures market prices, ICF believes that the producers in economic dry gas plays like the Marcellus and Haynesville plays will be incentivized to complete their inventory of drilled but uncompleted (DUC) wells, and/or increase their drilling activity—thereby offsetting the production decline and limiting the increase in natural gas prices.

Natural gas demand expected to decline

ICF expects significant reductions in near-term natural gas demand in response to the COVID-19 pandemic. While we expect residential demand to remain relatively unchanged, we project peak losses of roughly 1 billion cubic feet per day (Bcf/d) of commercial demand, 2 Bcf/d of industrial demand, 2 Bcf/d of demand for feedgas for liquefied natural gas (LNG) for exports, and 0.5 Bcf/d of demand for pipeline exports to Mexico. The decline in industrial demand includes a significant reduction in refinery demand for natural gas as lower demand for transportation fuels and other petroleum products also erodes the demand for domestic refinery natural gas.

There is significant additional downside risk associated with LNG exports. While we have reduced our LNG export forecast by as much as 2 Bcf/d, U.S. LNG export costs are currently above international LNG prices, placing additional exports at risk. While LNG exports are supported by existing contracts, the price relationship between LNG (based on the Henry Hub price of gas) and competing sources of international LNG (indexed to the Brent crude oil price) currently favors international sources of LNG supply.

The rapid recovery of prices in the forward curve by July 2020 also appears to rely on the forecasts of a V-shaped recovery in economic activity and demand, which seems to us optimistic. A prolonged loss in U.S. domestic demand and export demand, combined with storage levels now back above the five-year average and without much loss in dry gas production, make the over $0.20/MMBtu increase in prices between June and July unlikely.

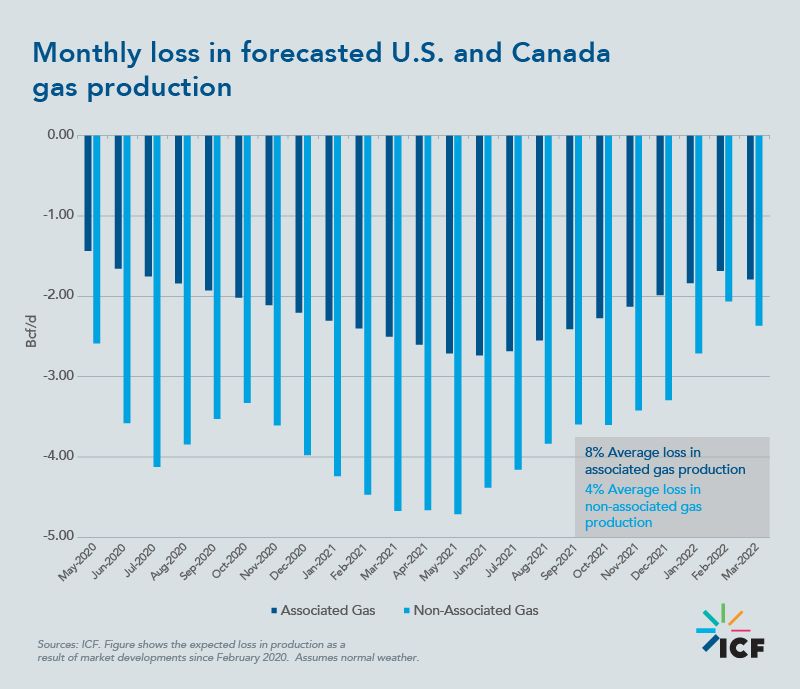

While we are hopeful for a rebound in demand by this winter, we expect natural gas storage levels going into the winter to be very high, holding down the potential for a significant rebound in gas prices. We expect U.S. and Canadian storage levels to be above 4.3 trillion cubic feet (Tcf) going into this winter, which will hold down prices—even as expected production losses hit 6.5 Bcf/d.

Demand could recover just as production potential is at its lowest

While lower oil prices will lead to reductions in associated gas production, ICF does not anticipate that those reductions will occur soon enough to cause the price impacts seen in this winter’s Henry Hub forward pricing. Instead, the larger impacts are likely to be during the following winter.

During the summer of 2021, when demand for natural gas globally and in the United States and Canada is expected to begin to recover more substantially, the loss in gas supply from capital expenditure reductions by oil and gas producers will be at its peak. As a result, ICF forecasts that storage levels could be 1 Tcf lower going into the winter of 2021/2022.

So, while production may be declining faster than demand, it is more likely that the recovery in natural gas demand and the loss of production combine to send gas above $3.00/MMBtu in the winter of 2021/2022 instead of the winter of 2020/2021.

In other words, as shown in ICF’s fundamentals-based forecast, the forward curves for the next two winters may need to be flipped.